GST Registration

Get your business GST-ready with a simple and hassle-free process.

2000

Happy Clients

1500

Expert Advisors

2+

Branch Offices

Free Consultation by Expert

.png)

.png)

.png)

GST Registration in Delhi - Get Your GSTIN in 3 Working Days

If you run a business anywhere in Delhi - a shop in Karol Bagh, a trading office in Chandni Chowk, a consultancy working out of Rohini or Pitampura, or an online store shipping from Dwarka - GST registration is the point where your business becomes formally visible to the tax system. Once registered, you get a 15-digit GSTIN. For Delhi, that number always starts with 07, which is Delhi's state code under GST.

This page covers who actually needs to register in Delhi, the documents you need to keep ready, the exact process, what it really costs, and the new 3-day route under Rule 14A that most people still do not know about. We have kept the numbers honest. Where a figure depends on your specific case, we have said so instead of quoting a made-up amount.

Get Started Today|

Talk to a Delhi GST expert before you apply. |

Who Needs GST Registration in Delhi

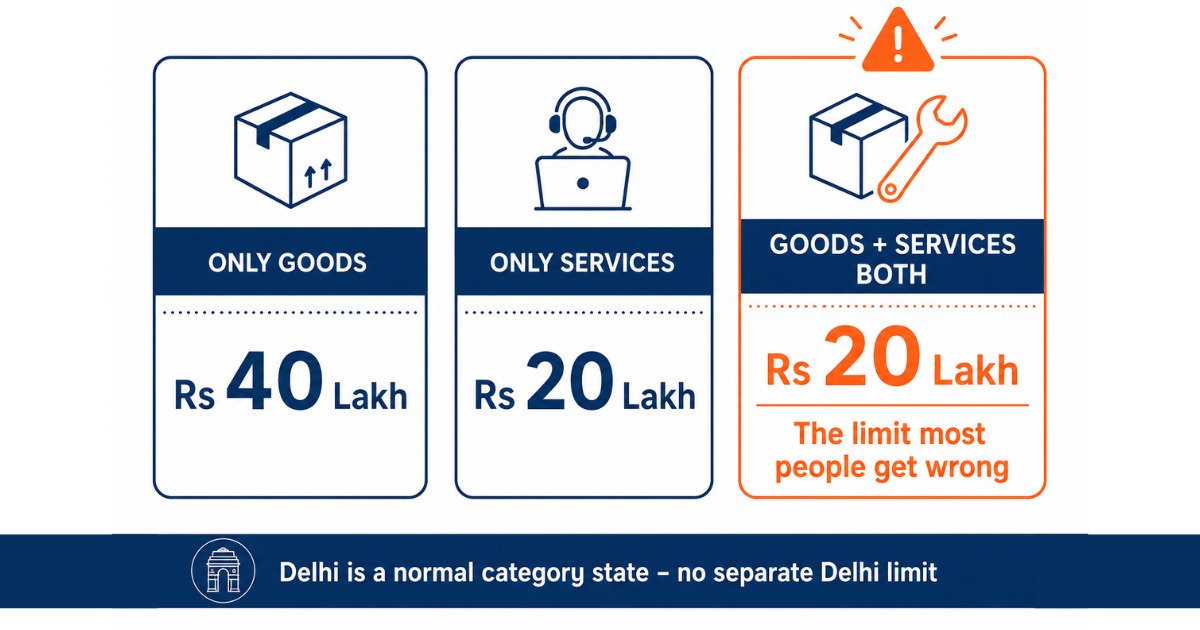

Delhi is a normal category state, not a special category state. So the standard national thresholds apply here - there is no separate, lower Delhi limit. This is worth saying plainly, because a lot of pages online confuse this.

| Your business type | Threshold in Delhi | What to watch for |

| Only goods | INR 40 lakh aggregate turnover |

Applies only if you deal purely in goods |

| Only services | INR 20 lakh aggregate turnover |

Most Delhi consultants, agencies and freelancers sit here |

| Goods and services both | INR 20 lakh aggregate turnover |

This is the one people get wrong - see the note below |

| The mixed-supply trap. Suppose you run a hardware shop in Delhi that also charges for installation and repair. You might assume the INR 40 lakh goods limit protects you. It does not. The moment you supply services alongside goods, the INR 20 lakh limit applies to your whole turnover. We see this catch Delhi businesses regularly, usually after they have already crossed the line. |

Also note that aggregate turnover is counted PAN-wise across all of India, not just your Delhi operations. If you run a consultancy in Delhi and also earn rental income from a property elsewhere under the same PAN, both count toward the same limit.

When You Must Register Regardless of Turnover

Section 24 of the CGST Act overrides the threshold entirely for certain categories. If you fall in any of these, turnover is irrelevant - you register from day one:

- You supply goods from Delhi to customers in other states

- You are a casual taxable person - for example, a stall at an exhibition at Pragati Maidan

- You are a non-resident taxable person supplying into Delhi

- You are required to deduct TDS or collect TCS under GST

- You are an Input Service Distributor

- You pay tax under reverse charge

| An important correction on e-commerce. Many Delhi pages still say every online seller must register from the first rupee. That has not been fully true since 1 October 2023. A small seller of goods can stay unregistered if they sell only within Delhi, stay under the threshold, sell through e-commerce operators in one state or union territory only, and declare their PAN and place of business on the GST portal. The moment you ship outside Delhi, registration becomes mandatory. In practice almost every Delhi seller on Amazon or Flipkart ships nationally, so they do need it - but the rule is not what most sites claim, and you should know which side of it you are on. |

On inter-state services, there is a further point worth knowing. A Delhi consultant billing a Mumbai client does not need registration simply because the client is in another state. The normal INR 20 lakh threshold still protects small service providers. The compulsory inter-state rule bites on goods, not on small service supply.

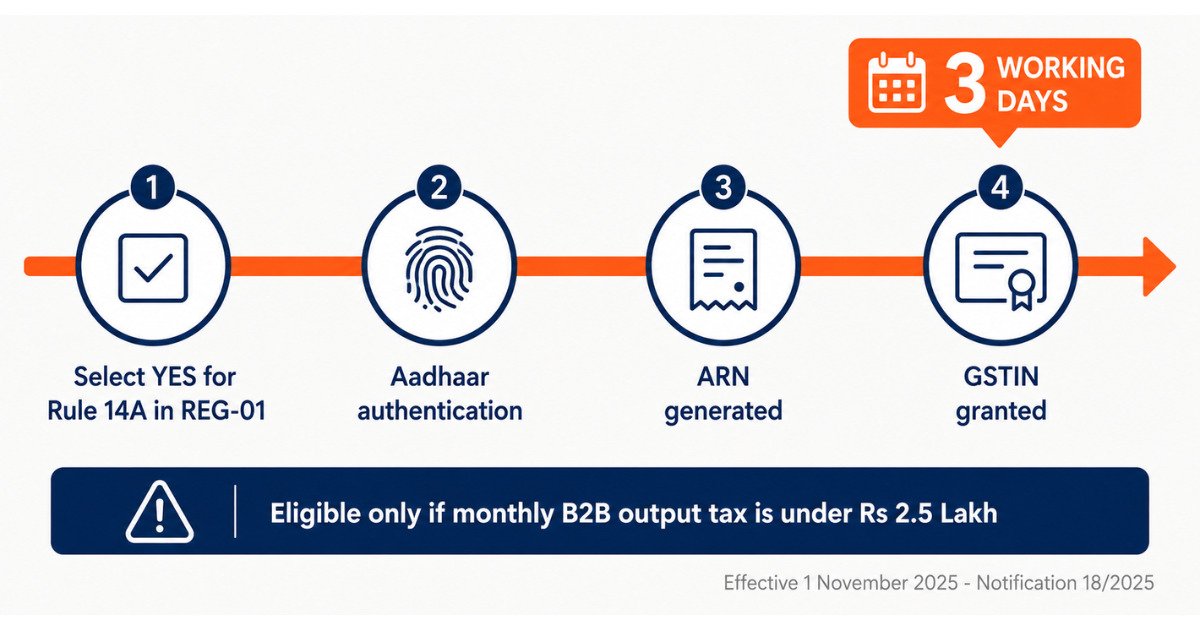

The 3-Day Route: Simplified GST Registration Under Rule 14A

This is the biggest change to GST registration in years, and almost no Delhi page mentions it.

Rule 14A was inserted into the CGST Rules by Notification No. 18/2025 - Central Tax, effective 1 November 2025. It creates an optional fast-track route where registration is granted electronically within three working days of your ARN being generated, subject to Aadhaar authentication.

Who Can Use It

| 1 | Your self-assessed monthly output tax liability on supplies to registered persons (B2B) is not expected to exceed INR 2.5 lakh per month, including CGST, SGST, IGST and cess |

| 2 | You do not already hold another Rule 14A registration in Delhi under the same PAN |

| 3 | Aadhaar authentication is completed for the Primary Authorised Signatory and at least one Promoter or Partner |

To use it, you select "Yes" against the Rule 14A option in Form GST REG-01. If you do not select it, you go down the standard route.

The Part Nobody Warns You About

Rule 14A is genuinely faster, but exiting it is not trivial. If you later grow past the INR 2.5 lakh monthly B2B liability, you have to withdraw using Form GST REG-32, and the officer passes an order in Form GST REG-33. Before you can withdraw:

- All returns from your registration date to the withdrawal date must be filed

- If you apply on or after 1 April 2026, at least one tax period's return must be filed

- No amendment or cancellation application may be pending

- No proceedings under Section 29 may be running

| Our honest read: if you are a small Delhi service provider or B2B supplier who will comfortably stay under INR 2.5 lakh monthly output tax, Rule 14A is worth taking. If you expect to scale quickly past it, the standard route avoids a withdrawal process you will have to manage later. This is exactly the kind of judgement call worth a five-minute conversation before you tick the box. |

Documents Required for GST Registration in Delhi

The document list changes with your business structure. Here is what is actually needed, rather than one generic list.

| Proprietorship / Individual |

|

| Partnership / LLP |

|

| Private Limited / OPC |

|

Address Proof - Where Delhi Applications Actually Fail

This is the single biggest cause of rejections and REG-03 queries in Delhi, so it deserves its own section.

| Your premises | What you need |

| Owned | Latest electricity bill, or property tax receipt, in the owner's name |

| Rented | Registered rent agreement plus the landlord's latest electricity bill |

| Relative's or consent property | No Objection Certificate from the owner, plus their electricity bill and ownership proof |

Practical points that matter in Delhi specifically:

- A commercial address is not mandatory. Home-based businesses in Rohini, Dwarka, Janakpuri or anywhere else in Delhi can register on a residential address with valid proof. Do not let anyone tell you otherwise to sell you an address.

- The name on the electricity bill must reconcile with your paperwork. A bill in a deceased parent's name, or in a previous tenant's name, is the classic Delhi rejection. Fix this before applying, not after.

- Be careful with virtual offices. Virtual office addresses are heavily scrutinised in Delhi, and CBIC's verification instructions of April 2025 tightened physical verification of premises. If the officer visits and finds no genuine place of business, you are looking at rejection or later cancellation. If you genuinely operate from a virtual office, be ready to defend it with a proper agreement and NOC.

GST Registration Process in Delhi - Step by Step

The whole thing is done online at gst.gov.in. You do not visit any GST office in Delhi, though you may need to visit a GST Suvidha Kendra if biometric authentication is triggered.

| 1 | Start Part A. Go to gst.gov.in, then Services, then Registration, then New Registration. Enter your PAN, mobile and email. Verify both OTPs. You get a Temporary Reference Number (TRN) - save it. |

| 2 | Log back in with the TRN and fill Part B. This is the long part: business constitution, principal place of business in Delhi, nature of premises, HSN codes for goods or SAC codes for services, promoter and director details, authorised signatory, and bank details. |

| 3 | Choose your Rule 14A option. Select "Yes" if you qualify and want the 3-day route. Think about this before you click - see the section above. |

| 4 | Upload documents. Clear scans, correct file sizes. Blurry uploads are a common trigger for queries. |

| 5 | Complete Aadhaar authentication. OTP-based is faster. Biometric authentication at a GST Suvidha Kendra is required in some cases. If you skip Aadhaar authentication altogether, expect physical verification of your Delhi premises and a much longer timeline. |

| 6 | Submit with DSC or EVC. Companies and LLPs must use a Class 3 DSC. Proprietors and individuals can use EVC. |

| 7 | Track your ARN. You get an Application Reference Number immediately. Track it on the portal. |

| 8 | Respond to any REG-03 query within 7 working days. If the officer wants clarification, you reply in Form GST REG-04. Missing this window is how applications die. |

| 9 | Receive your GSTIN and download Form REG-06 - your registration certificate - from the portal. |

After You Get the GSTIN - the 30-Day Bank Account Rule

| This catches new Delhi registrants constantly. Under Rule 10A, you must furnish valid bank account details linked to your business PAN within 30 days of registration being granted, or before filing your first GSTR-1 or IFF, whichever is earlier. Miss it and your registration can be suspended. Getting the GSTIN is not the finish line. |

GST Registration Fees in Delhi

Let us be straight about this, because the pricing on this topic is full of noise.

| Cost head | Amount | Notes |

| Government fee for GST registration | INR 0 | The GST portal charges nothing. Anyone quoting a government fee is misleading you. |

| Professional / consultancy charges | Varies by structure | A proprietorship is simpler than a Pvt Ltd with multiple directors and DSC handling. Ask for a written quote. |

| Class 3 DSC, if required | Extra, if you do not already have one | Needed for companies and LLPs. Proprietors using EVC do not need it. |

| Notarised rent agreement or NOC | Extra, if applicable | Depends on your premises situation |

We have deliberately not printed a single headline price here. Your actual cost depends on your structure, whether you need a DSC, and whether your address paperwork is clean. Call us and you will get a real number for your case, not a teaser rate that changes at checkout.

How Long Does GST Registration Take in Delhi

| Route | Timeline |

| Rule 14A simplified route, Aadhaar authenticated | 3 working days from ARN generation |

| Standard route, Aadhaar authenticated, clean documents | Around 3 to 7 working days |

| Without Aadhaar authentication | Substantially longer - physical verification of premises is likely |

| If a REG-03 query is raised | Add the time you take to reply, plus officer review |

Benefits of GST Registration for a Delhi Business

| Input Tax Credit. You offset GST paid on your purchases - office rent, supplies, raw material - against GST collected from customers. For most Delhi businesses this is the real financial argument. |

| B2B credibility. Corporate clients and government departments need a valid GSTIN on your invoice to claim their own ITC. Without it, many will simply not deal with you. |

| Selling outside Delhi. Delhi's position in the NCR trade network means most growing businesses supply outward. A GSTIN removes the barrier. |

| E-commerce access. Selling nationally on Amazon, Flipkart or Meesho from a Delhi base requires it. |

| Government tenders. A valid GSTIN is standard eligibility criteria. |

| Current account and credit. Banks treat a GST certificate as legitimate business proof. |

Penalty for Not Registering in Delhi

| What you did | What it costs |

| Failure to register when liable | 10 percent of the tax due, minimum INR 10,000 |

| Deliberate evasion | Up to 100 percent of the tax due, under Section 122 of the CGST Act |

| Interest | On the tax that should have been collected |

| There is a further point people miss. If you register late, your effective registration date is when the officer grants it - not when you crossed the threshold. The gap period still carries tax liability, and you cannot go back and collect that GST from customers you have already billed. It comes out of your own pocket. That is usually the expensive part, not the penalty itself. |

Delhi GST Jurisdiction - Which Department Handles You

Delhi taxpayers fall under a dual control structure. For turnover up to INR 1.5 crore, administrative jurisdiction generally sits with the Delhi State GST department (Department of Trade and Taxes, GNCTD). Above that, jurisdiction is shared between the Central GST authorities and Delhi SGST. This determines who contacts you for audits, notices and refund processing. Your ward and range are assigned based on your principal place of business address in Delhi.

Areas We Cover Across Delhi

The process is fully online, so we handle GST registration for businesses across all of Delhi. You do not need to travel to us and we do not need to visit you.

| Rohini | Pitampura | Samaypur Badli |

| Dwarka | Janakpuri | Karol Bagh |

| Laxmi Nagar | Connaught Place | Chandni Chowk |

| Nangloi | Shahdara | Okhla |

| Netaji Subhash Place | Rajouri Garden | Saket |

|

Not sure whether you cross the threshold, or whether Rule 14A suits you? That conversation is free, and it takes five minutes. |